Draft Accounting Circular 2026 – Key Updates Sole Proprietorships Must Pay Attention To

Nội dung

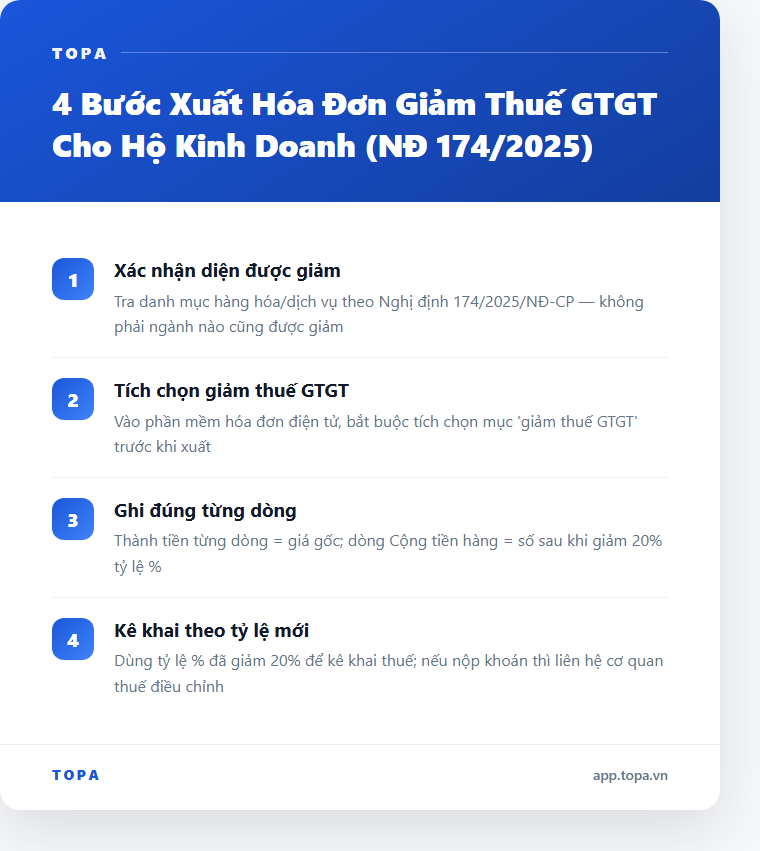

1. Overview of the Draft Circular

Recently, the Ministry of Finance announced that it is seeking public feedback on the Draft Circular guiding accounting for sole proprietorships and individual business households — expected to take effect on January 1, 2026, replacing Circular 88/2021/TT-BTC.

According to the summary, the Circular includes:

- Chapter I (Articles 1–3): General provisions (scope – applicable entities; organization of accounting work; retention of accounting documents)

- Chapter II (Articles 4–10): Detailed rules by revenue group and tax method for each category of sole proprietorships and individual business households.

- Chapter III (Article 11): Implementation and effective date.

From the perspective of a chief accountant, I believe this is a significant “standardization step”: whereas sole proprietorships previously operated under simplified rules, they will now be required to standardize bookkeeping, storage, and revenue classification. For existing business households, reviewing and preparing early is essential — because “there will be no turning back” once the Circular becomes effective.

2. Key updates sole proprietorships must know

2.1 Group 1: Annual revenue ≤ VND 200 million

According to the Draft, if a sole proprietorship or individual business has annual revenue of VND 200 million or less, the accounting regime is very simple: they only need to use the Detailed Sales Revenue Ledger (Form S1a-HKD) to record revenue.

Cost/expense transactions will not require detailed bookkeeping like in larger enterprises — which is clearly a procedural relief. However, I must emphasize: this does not mean invoices and supporting documents are unnecessary, as tax audits may still require them.

This helps households with small revenue comply more easily — but if their activities grow beyond this threshold, they must move to Group 2 with more complex bookkeeping requirements.

2.2 Group 2: Revenue > VND 200 million ≤ VND 3 billion

This group is divided into two cases:

- Sole proprietorships paying VAT and PIT based on a percentage of revenue → use Form S2a-HKD (Detailed Sales Revenue Ledger) to record revenue by business line.

- Sole proprietorships paying VAT under the credit method and PIT based on a percentage of revenue → use both S2a-HKD and S2b-HKD (Ledger for monitoring VAT obligations to the State Budget).

I note that this group is the “middle step” — meaning once revenue exceeds VND 200 million, detailed bookkeeping by form and industry classification is required. This may be challenging for those who self-manage their accounting without preparation.

If using the VAT credit method, they must also track input/output invoices and input VAT — a shift closer to enterprise-level accounting rather than simplified household accounting.

2.3 Group 3: Revenue > VND 3 billion

For households with annual revenue over VND 3 billion, the Draft sets out two cases:

- Paying VAT as a percentage of revenue & PIT based on taxable income → use Forms S3a-HKD (detailed revenue & expenses) and S2a-HKD (sales revenue).

- Paying VAT under the credit method & PIT based on taxable income → must use multiple ledgers: S2b-HKD, S3a-HKD, S3b-HKD (materials, tools, goods), and S3c-HKD (cash details).

Notably, the Draft also allows households with revenue above VND 3 billion to apply the accounting regime for micro-enterprises.

Thus, once revenue exceeds VND 3 billion, the line between “sole proprietorship” and “small enterprise” becomes blurry — requiring bookkeeping, accounting skills and documentation similar to small businesses.

2.4 Property leasing and e-commerce activities

Article 9 provides special rules for households with property leasing or e-commerce activities: if they pay VAT and PIT based on a percentage of revenue, they use the same ledger as in Article 5 (Form S2a-HKD).

This is important as many households are now expanding into leasing (houses, shops, equipment) or selling via e-commerce platforms — previously unclear in terms of bookkeeping but now covered under explicit rules.

2.5 Sole proprietorships subject to special taxes

According to Article 10, households engaged in activities subject to special taxes (export/import tax, excise tax, natural resources tax, environmental protection tax, land use tax) must prepare an additional ledger: Special Tax Obligations Ledger, besides the revenue-group ledgers.

For households in industries subject to these taxes (e.g., real estate leasing, specialized equipment, imported goods), this requirement is not merely an addition — it could represent a shift toward a small-enterprise model due to increased control and documentation.

2.6 Organizing accounting work & document retention

Article 2 states that the representative of the sole proprietorship may:

- Self-record the accounting books,

- Assign a staff member,

- Or hire an accounting service.

Family members (parents, spouse, adopted children) or warehouse/cashier staff may concurrently serve as accountants.

Regarding retention: the Draft requires that accounting documents (paper or electronic) be stored in accordance with the retention periods and formats issued by the Ministry.

This is an important point: many small households currently “record loosely or store documents chaotically” — from 2026, standardization is required. Professional accounting services (e.g., 1ketoan.com) can help reduce risks.

3. Practical impacts – risks & opportunities

Risks if unprepared

- If revenue exceeds a threshold but the household still applies a lower-group bookkeeping regime, it is at risk of audits, back taxes, and penalties.

- E-commerce or property leasing activities without proper ledgers may be considered “non-compliant”.

- Improper document retention (e.g., incorrect electronic formats) can create issues during internal audits or tax inspections.

- Self-managed accounting without understanding the new forms may lead to errors, re-filing, and reputational/tax risks.

Opportunities if well-prepared

- Even Group 1 households can build a strong “accounting management system” early, facilitating expansion.

- Standardization increases credibility with banks and partners.

- With professional support, households can optimize operating costs and avoid errors.

- Clear revenue group thresholds enable proactive planning — e.g., preparing for Group 3 before exceeding VND 3 billion.

4. What sole proprietorships should do before 01/01/2026

5. Conclusion & recommendations

The transition to the self-declaration – self-payment model in 2026 is undoubtedly a major turning point for household businesses. Many worry: What if I file incorrectly? What if I lack documents and get penalized? Will compliance costs increase substantially? These concerns are completely understandable, especially as regulations are changing quickly.

However, from a long-term perspective, the new model brings tangible benefits: more transparent financial records, better access to credit, and easier scaling — even transforming into a formal enterprise. Most importantly, you gain autonomy in tax calculation, reducing the previous “pay-as-requested” situation.

The biggest hesitation remains cost and risk. Is there a way to transition smoothly, affordably, and safely under the new regulations?

In reality, yes. With a knowledgeable support provider that stays updated and guides you step-by-step, preparing documentation and bookkeeping becomes much easier.

Many households undergoing this transition share that working with firms like 1ketoan from the beginning helped them avoid mistakes, control costs, and feel more confident when shifting to the new model. Sometimes, just a few early, accurate, and clear pieces of advice can save millions in compliance costs.

Approval of the Scheme on Transforming the Tax Administration Model for Household Businesses

Overview of Tax Obligations for Household Businesses in 2025

Common Issues with Tax Authorities for Software Manufacturing Enterprises