Regulations on Dependent Registration under the Latest Decision No. 216/QĐ-BTC

On February 3, 2026, the Ministry of Finance issued Decision No. 216/QĐ-BTC (2026), announcing amended, supplemented, and abolished administrative procedures in the field of tax administration under its authority.

This Decision officially took effect on February 14, 2026, introducing several important changes to tax procedures, including the abolition of the procedure for registering dependents for family circumstance-based deductions.

This is a matter of significant interest to individuals, businesses, and accountants, as dependents directly affect the amount of personal income tax payable. Keeping up to date with the latest regulations helps taxpayers fulfill their obligations accurately while avoiding unnecessary administrative procedures.

Nội dung

Detailed Provisions

Pursuant to Subsection 2, Section 1, Part I of the Appendix issued together with Decision No. 216/QĐ-BTC (2026) on the list of abolished administrative procedures under the Ministry of Finance’s authority, a key change has been applied to dependent registration procedures.

Accordingly, from February 14, 2026:

- The procedure for registering dependents for family circumstance-based deductions (administrative procedure code: 2.002229) for individuals earning income from salaries and wages is officially abolished.

- This procedure is replaced by the initial tax registration procedure applicable to individual taxpayers and their dependents (procedure code: 1.008489).

This change reflects the tax authority’s direction toward simplifying administrative procedures and synchronizing tax registration data, rather than maintaining multiple separate procedures for different purposes.

In practice, this means that dependent information will be managed directly through the tax registration system, reducing manual declarations and minimizing duplication of information.

Family Circumstance-Based Deduction Levels in 2026

The family circumstance-based deduction is the amount deducted from taxable income before determining personal income tax liability.

According to Clause 1, Article 19 of the Law on Personal Income Tax 2007, as amended by Resolution No. 954/2020/UBTVQH14:

“Family circumstance-based deductions are amounts deducted from taxable income before tax calculation for income from business, salaries, and wages of resident individual taxpayers. These deductions include:

- 11 million VND/month (132 million VND/year) for the taxpayer;

- 4.4 million VND/month for each dependent.”

However, from January 1, 2026, the deduction levels have been adjusted under Article 1 of Resolution No. 110/2025/UBTVQH15:

“Article 1. Family circumstance-based deductions for personal income tax

The deduction levels stipulated in Clause 1, Article 19 of the Law on Personal Income Tax are adjusted as follows:

a) 15.5 million VND/month (186 million VND/year) for the taxpayer;

b) 6.2 million VND/month for each dependent.”

Thus, from 2026 onward:

- 15.5 million VND/month applies to the taxpayer;

- 6.2 million VND/month applies to each dependent.

This adjustment is considered more aligned with current living costs and helps reduce the tax burden on employees.

- A spouse may qualify as a dependent if meeting the conditions under relevant regulations.

Parents and relatives:

- Biological parents;

- Parents-in-law;

- Stepparents;

- Legally adoptive parents.

Other individuals:

- Siblings;

- Grandparents (paternal and maternal);

- Aunts, uncles;

- Nephews/nieces (children of siblings);

- Other individuals directly supported by the taxpayer in accordance with the law.

Correctly identifying eligible dependents is crucial to ensuring accurate personal income tax calculation.

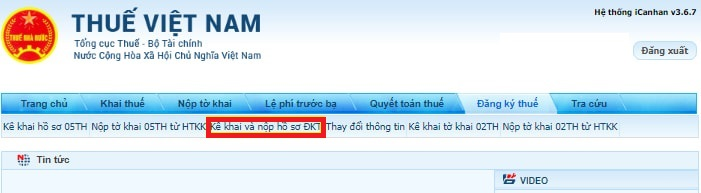

Case 1: Individual Self-Registration Online

- Access the website: thuedientu.gdt.gov.vn and log in to the personal e-tax account.

- Enter tax code, password, and verification code.

- Select “Tax Registration” → “Declare and submit tax registration dossier.”

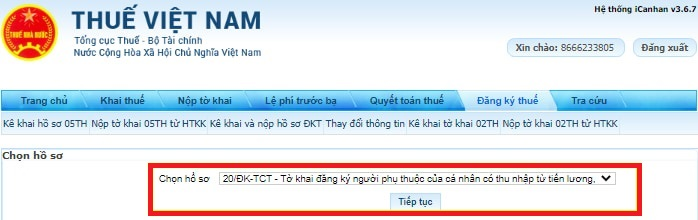

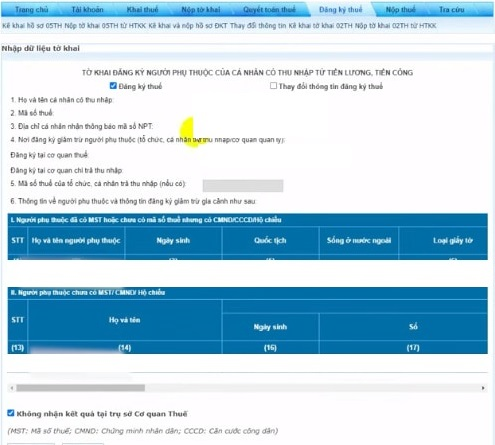

- Choose form “20-ĐK-TCT – Consolidated tax registration declaration for dependents of individuals earning salary/wage income.”

- Fill in the required information.

- Select “Complete declaration” → “Submit tax registration dossier.”

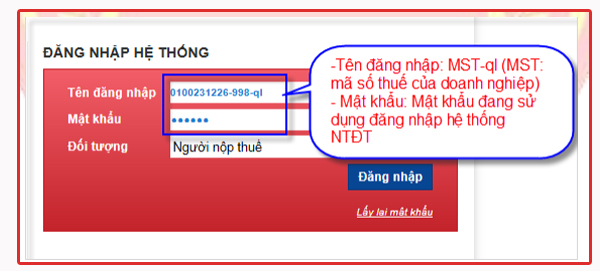

Case 2: Registration via Income-Paying Organization

- Access thuedientu.gdt.gov.vn and log in to the enterprise e-tax account.

- Enter tax code, password, and verification code.

- Select “Tax Registration” → “New registration/Change of individual information via tax authority.”

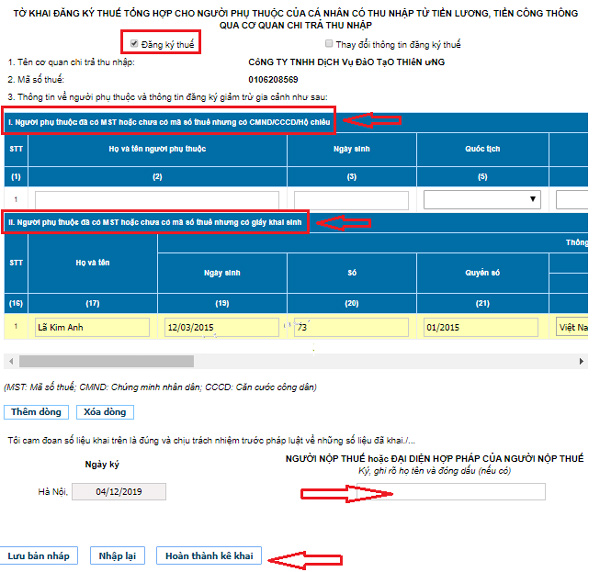

- Choose form “20-ĐK-TH-TCT_TT105…”

- Complete the declaration form.

- Enter the name of the director/legal representative.

- Select “Complete declaration” → “Submit dossier.”

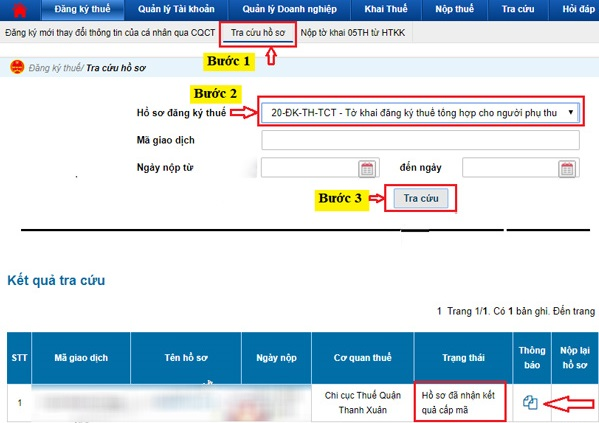

- Check status under “Tax registration dossier lookup.”

Processing time typically ranges from a few minutes to several hours if no errors are found.

Significance of the Change from 2026

The abolition of the separate dependent registration procedure under Decision No. 216/QĐ-BTC is a step toward simplifying administrative processes in tax management.

Instead of requiring a separate procedure for deductions, dependent information is now centrally managed within the tax registration system. This helps to:

- Reduce administrative paperwork for taxpayers;

- Improve data synchronization in tax management systems;

- Minimize errors and duplication of dependent information.

In the context of ongoing digital transformation in the tax sector, these changes enhance efficiency and make tax compliance more convenient.

Conclusion

From February 14, 2026, under Decision No. 216/QĐ-BTC, the procedure for registering dependents for family circumstance-based deductions has been officially abolished and replaced by the initial tax registration procedure for individuals and their dependents.

At the same time, deduction levels have been increased to:

- 15.5 million VND/month for taxpayers;

- 6.2 million VND/month per dependent.

Understanding these updated regulations helps both individuals and businesses comply with tax obligations while ensuring their lawful benefits in personal income tax finalization.

Update on Tax Authority Addresses in Thai Nguyen After Administrative Restructuring